You probably know a poor credit score can launch your mortgage rate sky-high. Did you know it can do the same to your homeowners insurance rate?

“If you have a fair credit score, you may pay 36 percent more for home insurance than someone with excellent credit,” concludes a recent study by InsuranceQuotes.com. “What’s more, if you have poor rather than excellent credit, your premium more than doubles, increasing by an average of 114 percent.”

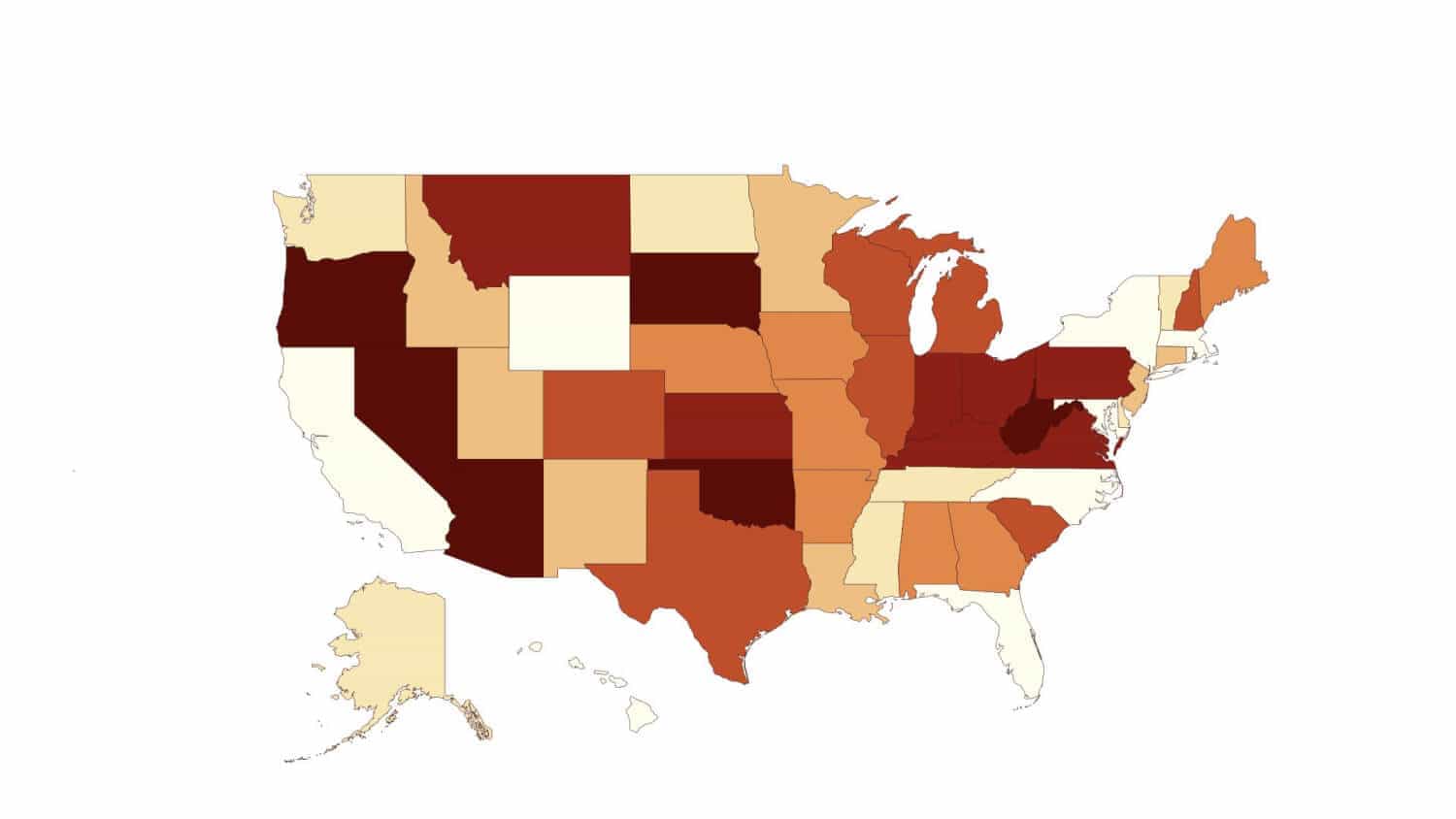

Actually, those are just averages. The size of the financial hit varies by state, as you can see here…

If you want a shock, look at South Dakota. A poor credit score there can hike your homeowners insurance rate by a stunning 288 percent.

The sad fact is, a poor credit score will hurt you much more today than decades ago. When I first became a CPA and a financial counselor, credit scores were reserved mainly for mortgages, car loans, and credit card accounts. Today, you might not be able rent an apartment or even get a job without someone reviewing your credit score.

The InsuranceQuotes.com study relied on something called credit-based insurance scores.

“Credit-based insurance scores are used by almost every insurance company in the nation because it’s a very good segmentation tool,” says Lamont Boyd, an insurance underwriting expert at FICO, which keeps the best-known credit scores of them all. “It’s such a powerful tool because it is very, very predictive of future losses.”

In other words, if you have a low credit score, you’re more likely suffer more insurance losses. That means you’re a more costly client, so insurers will charge you more.

The flip-side is also true. If you want to save up to two-thirds on your homeowners insurance and more, bulk up your credit score. First, however, you need to understand how credit scores work.

Understanding credit scores

As I alluded to above, the granddaddy of all credit scores is called your FICO credit score.

“Since all other scores are usually based at least somewhat on FICO, that means understanding your FICO credit score means you understand how to improve your credit,” Debt.com explains in its report, Understanding Your FICO Credit Score.

Most of your FICO is based on just two factors. Your payment history (35 percent) and how much debt you owe (30 percent). If you pay your bills on time and lower your overall debt, you can raise your score and save big on a range of financial tools.

Of course, that’s easier said than accomplished. If you struggle with debt already, it might be time for an expert opinion. Credit counseling is free and can point you to a path out of debt. What’s the catch? Well, it’s not a catch but it is a drawback in our fast-paced society: There is no quick fix.

It probably took you awhile to get deep into debt, so getting out will take at least as long. We’re talking months and even years. However, during that time, you can see marked improvements in your credit score.

For instance, if your credit cards are the problem, a debt management program can cut your total payments by 30 or even 50 percent. It also consolidates all your credit card bills into one monthly payment, which means your “payment history” improves.

If you learn anything today, I hope it’s this: Debt doesn’t just cost you now, it costs you later, and in ways that aren’t obvious. Thankfully, getting out of debt can save you now and later. If you wait to solve this thorny problem, you’re simply paying more for nothing.